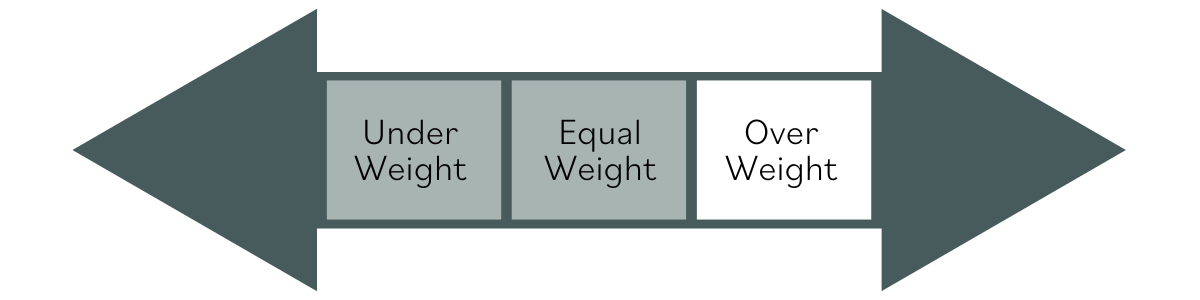

Our current stock allocation is in an Over Weight position. This allocation of stocks vs. bonds is driven by technical market signals. These signals may lead to a shift in stock weightings in SFMG portfolios’ target allocations. This is not meant to be a specific allocation recommendation as this may vary across client portfolios.

- The government-shutdown-delayed September payrolls report showed a solid gain of 119k jobs, beating expectations, though cumulative revisions of -33k for August and July weakened the headline strength. The unemployment rate ticked up from 4.3% to 4.4%, marking its highest level in four years. Overall, the report offered a mixed signal, pairing resilient hiring with signs of a gradually cooling labor market.

- The Trump administration removed steep tariffs on a wide range of Brazilian agricultural goods in November, including beef and coffee, reversing duties imposed earlier this summer. Brazil is a major supplier of fruit juices, sugar, beef, and coffee to the U.S., and the action is part of a broader effort to address rising food costs affecting American consumers. The move also mirrors a framework announced earlier in the month to eliminate reciprocal tariffs on more than 200 products worldwide.

- U.S. consumer sentiment, measured by the University of Michigan Consumer Sentiment Index, fell 2.6 points to 51.0 in November, the second-lowest reading ever, and down 29% from a year ago. Consumers remain frustrated by high prices and weaker incomes, while labor market concerns also persist.

- The S&P 500 opened 1.55% higher on November 20 following Nvidia’s strong earnings report but reversed sharply to close down 1.52%. The selloff was driven by rising concerns around the sustainability of AI-driven demand and renewed uncertainty over the Fed’s rate-cut path. Such intraday reversals of this size are historically rare, underscoring the market’s heightened sensitivity to shifting narratives.

- As of November 20, Consumer Discretionary, Consumer Staples, and Real Estate occupy the bottom of the S&P 500’s year-to-date sector rankings, with Consumer Discretionary down 0.7%. If these standings persist, it would be the first time since 1990 that Consumer Discretionary ends the year as the weakest sector—and the first time both consumer-oriented groups simultaneously finish among the three worst performers—suggesting the market may be tempering expectations for household demand.

- Artificial Intelligence hyperscalers like Meta, Amazon, Alphabet, and Oracle have begun to issue massive bonds to finance growth initiatives. This subset has issued nearly $90 billion of investment-grade bonds since September. Credit markets have been cautious. Some of the issuers had to pay higher interest rates than expected and even after issuance, prices for these bonds in the secondary market have slid.

Lower-income households continue to have both the highest share—and the largest increase—of those living paycheck to paycheck. In 2025, 29% of lower-income households report living paycheck to paycheck, up from both 2024 and 2023, while the shares among middle- and higher-income households have changed little. The primary reason is slower wage growth among lower-income workers. This group saw the strongest income gains in 2021-22, but that momentum has faded. At the same time, inflation has reaccelerated, further widening the gap between income and expenses for these households.

During the first quarter, non-U.S. equities outperformed the U.S. market amid tariff-related volatility, after which U.S. equities outperformed for several months following the resolution of those tensions. Since August, however, non-U.S. stocks have begun to modestly outperform the U.S. market again. With U.S. benchmarks like the S&P 500 becoming increasingly concentrated and driven by only a few large tech names—where valuations have raised concerns—investors may be seeking greater diversification and more attractive valuations. The S&P 500 is roughly flat over the past two months (9/22/25 – 11/24/25), up 0.17%, while the All-Word ex US index (proxy ticker: ACWX) is up 4.18%.

Although the record-long government shutdown has ended—at least until the current funding resolution expires in late January—market volatility picked up in November. AI stocks and the broader market saw a sharp but contained pullback, unwinding part of a six-month rally. Semiconductors and mega-cap tech led the decline amid worries about an AI bubble, stretched valuations, crowded positioning, and uncertainty over how quickly AI investment will translate into earnings. Shifting expectations for Fed rate cuts are also contributing to volatility, especially as policymakers respond to incomplete labor and inflation data following the shutdown. The lack of timely data has made it harder to gauge whether labor-market softening warrants faster cuts or whether sticky inflation should keep rates steady. At the same time, the economy is showing an increasingly “K-shaped” pattern. Higher-income households continue to spend, supported by low unemployment, stronger wage growth, and significant stock-market wealth. Lower-income households, however, face rising unemployment and much weaker wage gains—after-tax income rose just 1.0% YoY, compared with 2.0% for middle-income and 3.7% for higher-income groups—leaving a wide and persistent gap. Because higher-income consumers account for most U.S. spending and hold a disproportionate share of equities, their financial health remains central to the outlook. But if the AI-driven market rally falters, the resulting market weakness could have a more direct impact on consumer spending than usual, given how closely this group’s confidence is tied to equity-market gains. Upcoming holiday spending data will offer a valuable pulse on this dynamic—revealing whether strength among higher-income households can continue to offset growing pressures on lower-income consumers and provide insight on how Americans across the income spectrum are truly faring.

The purpose of the update is to share some of our current views and research. Although we make every effort to be accurate in our content, the data is derived from other sources. While we believe these sources to be reliable, we cannot guarantee their validity. Charts and tables shown above are for informational purposes, and are not recommendations for investment in any specific security.