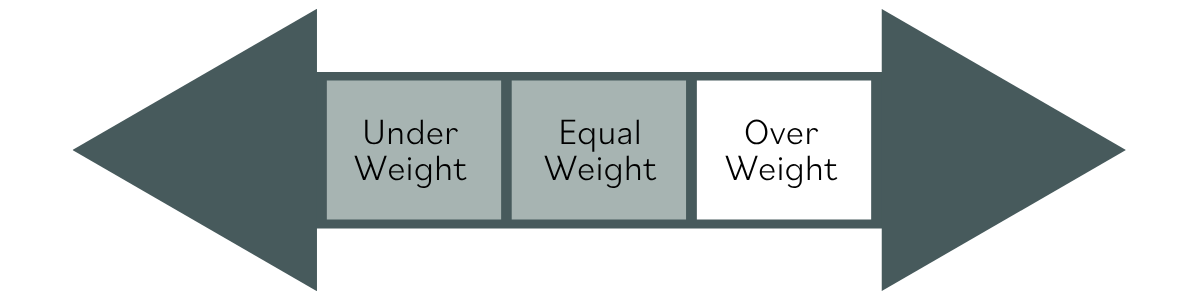

Our current stock allocation is in an Over Weight position. This allocation of stocks vs. bonds is driven by technical market signals. These signals may lead to a shift in stock weightings in SFMG portfolios’ target allocations. This is not meant to be a specific allocation recommendation as this may vary across client portfolios.

- Kevin Warsh was sworn in Friday at the White House as the 17th Chair of the US Federal Reserve, marking the first time since Alan Greenspan in 1987 that a Fed chair has taken the oath there. Warsh is expected to make significant changes to the Fed’s use of its balance sheet as a policy tool and to revamp the central bank’s communication strategy. Ahead of the ceremony, Fed Governor Christopher Waller, generally viewed as one of the more dovish FOMC members, said he favors removing the easing bias from the Fed’s policy statement and acknowledged that inflation trends are moving in an unfavorable direction.

- April inflation came in hotter than expected across both Consumer Price Index (CPI) data, which measures changes in prices paid by consumers, and Producer Price Index (PPI) data, which tracks price changes received by producers and businesses. The Iran conflict contributed to the pressure. CPI rose 0.6% for the month, driven by higher energy and shelter costs, while PPI jumped 1.4%, pushing annual producer inflation to its highest level since late 2022. “Core” readings which exclude energy and food prices also exceeded expectations, suggesting inflation pressures are broadening beyond just energy.

- The latest round of China’s April economic data pointed to a much sharper slowdown than expected, raising the likelihood of additional policy support later this year as the government works to maintain its 4.5%–5% growth target. Retail sales, fixed asset investment, and even industrial production either fell or posted their weakest growth rates in years. Poor weather conditions in parts of the country, along with reported methodological changes, may have contributed to the softer-than-expected results.

- The 30-year US Treasury yield climbed to 5.19%, its highest level since 2007. But it’s not just U.S. rates that are rising. UK government bond yields also moved higher amid political and inflation concerns. The rise in yields is increasingly being driven by broader global inflation worries, not just higher oil prices. Higher rates can pressure stocks and raise borrowing costs for mortgages, auto loans, and credit cards, potentially weighing on consumer spending.

- Gold prices spiked dramatically in January, rising more than 20% as investors rushed into safe-haven assets amid escalating geopolitical and trade uncertainty, including tariff threats and broader policy volatility. Since peaking on 1/28/26, and even throughout the war with Iran, gold prices have fallen roughly 18%. Interest rates have been rising due to higher inflation expectations and a lower probability that the Federal Reserve will cut rates. On a relative basis, higher rates make gold less attractive compared to yield-generating investments such as bonds, which is likely adding to the downward price pressure.

- Cybersecurity stocks fell early in 2026 as investors worried AI could disrupt parts of the software and security landscape, while elevated valuations amplified the selloff, but they rebounded in April and May as the market shifted to viewing AI as a tailwind for security demand; for example, the First Trust Cybersecurity ETF (CIBR) is up 37.90% since its 4/10/26 low.

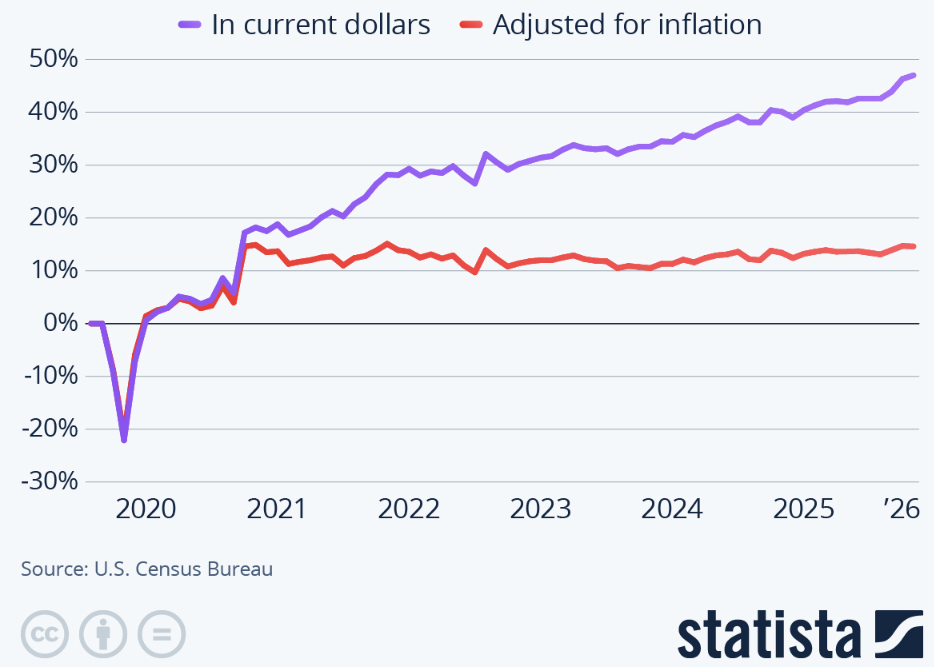

U.S. retail and food services sales rose 0.5% in April and were up 4.9% year over year, indicating that consumer spending remains resilient despite higher inflation. However, “real” retail sales (which means sales adjusted for inflation to reflect actual changes in purchasing power) were slightly negative in April, down about 0.1%, implying consumers paid more but bought roughly the same amount of goods. Over the past year, nominal sales outpaced inflation modestly, but over the past five years, most of the reported sales growth has been offset by higher prices—meaning households are spending significantly more in dollar terms just to maintain similar levels of consumption.

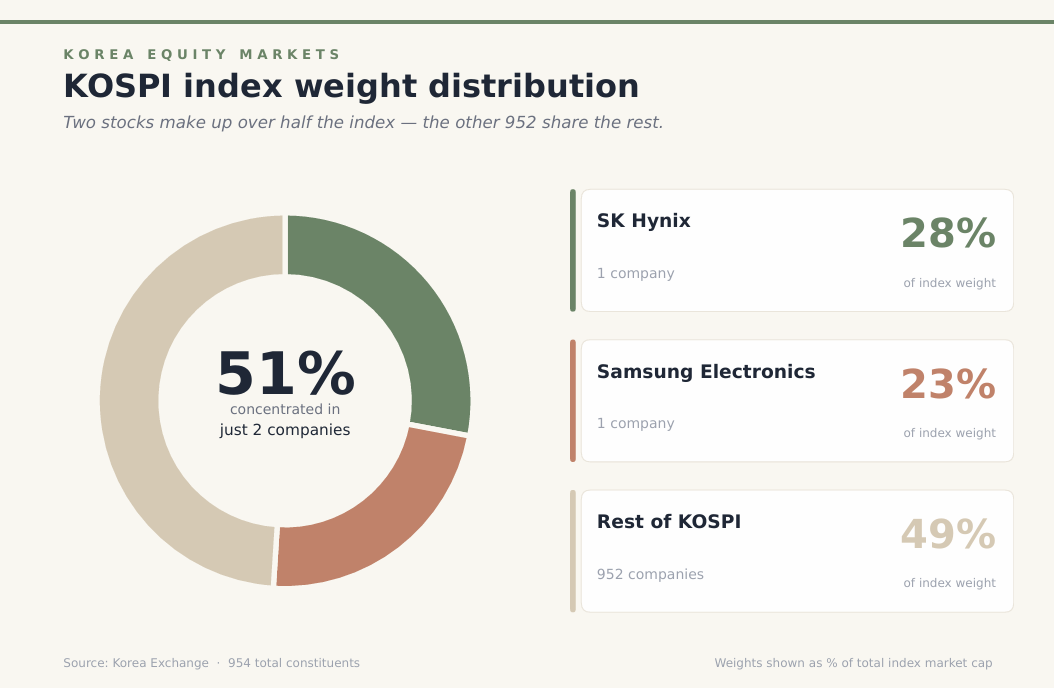

While we’ve noted the extreme concentration in the S&P 500, South Korea’s KOSPI index is even more risky. The KOSPI, the country’s main equity benchmark, has risen meaningfully over the past month, but that rally is heavily driven by a narrow group of stocks. Despite having 954 constituents, Samsung Electronics and SK Hynix together account for just over half the index, with SK Hynix at ~27.7% and Samsung at ~23.6%. Both companies are tied to the same AI-driven memory-chip cycle, particularly high-bandwidth memory (HBM) demand, making their performance highly correlated. This creates significant single-theme risk—if AI-related demand slows or either company disappoints on earnings, the impact would likely ripple through the entire index given how dominant these two names are.

The stock market continued to press higher in May as earnings figures continued to come in strong. US large-cap results were especially robust, building on an already solid prior quarter. S&P 500 earnings came in 16.3% above analyst expectations, with every sector beating estimates, while revenues also exceeded forecasts by 2.0%—both improvements versus last quarter. Small caps also delivered solid aggregate earnings, though breadth remains a weak spot, with only 6 of 11 sectors showing positive growth. Outside the US, earnings trends are also constructive. In Europe, 64% of the companies in the MSCI Europe Index beat first quarter earnings expectations, the highest in three years and well above historical norms, with the sharp improvement from the prior quarter historically associated with stronger future equity returns. Despite strong stock market performance, inflation remains a key overhang and could become more problematic if it persists. The tension is that markets are pricing in a relatively stable inflation path, while interest rates are increasingly reflecting a “higher-for-longer” reality—something that may not be sustainable alongside strong growth and rising stocks. Eventually, one of these has to give. In the near term, rates may continue to drift higher until that adjustment happens. There are pockets of softness in the US economy, particularly housing, but conditions are not deteriorating sharply—the NAHB homebuilder index even improved in May despite elevated mortgage rates. Meanwhile, labor indicators remain solid, with ADP’s data showing roughly 183k private jobs added in early May. Overall, the US economy has absorbed a series of shocks over the past year—including tariffs, constrained labor supply, and energy price spikes—yet remains resilient, supported by solid company spending, strong profits, and a still-functioning labor market.

The purpose of the update is to share some of our current views and research. Although we make every effort to be accurate in our content, the data is derived from other sources. While we believe these sources to be reliable, we cannot guarantee their validity. Charts and tables shown above are for informational purposes, and are not recommendations for investment in any specific security. Forward-looking statements are based on current expectations and assumptions and are subject to risks and uncertainties that may cause actual results to differ materially.