Our current stock allocation is in an Over Weight position. This allocation of stocks vs. bonds is driven by technical market signals. These signals may lead to a shift in stock weightings in SFMG portfolios’ target allocations. This is not meant to be a specific allocation recommendation as this may vary across client portfolios.

- The US and Iran reached an interim agreement to reopen the Strait of Hormuz, committing to an immediate halt of military operations and launching 60 days of negotiations on a final deal. While outstanding geopolitical issues remain, global markets have responded favorably to expectations that energy flows may normalize by late July and Persian Gulf crude production may recover by October.

- The European Central Bank (ECB) raised its key interest rate by 0.25% to 2.25% this month. This was the first increase since September 2023. This decision was driven by rising inflation pressures from elevated energy prices linked to Middle East tensions, which are expected to ripple through food, goods, and services pricing. Financial markets are pricing in two additional rate hikes throughout 2026 as the ECB continues to monitor inflation risks and their impact on the eurozone economy.

- The US job market showed strength in May with 172,000 jobs added, more than double expectations, while the unemployment rate remained stable at 4.3%. However, the data revealed some softness, including concentrated job gains in just a few industries, elevated long-term unemployment, and slowing wage growth at 3.4% year-over-year. While the labor market is recovering from late 2025’s slowdown, the Fed faces a delicate balancing act between supporting employment and managing inflation that remains elevated.

- In June, questions resurfaced about the enormous capital being deployed into AI data center infrastructure and whether companies will be able to demonstrate proportional returns in the near term. Against that backdrop, defensive sectors held up well during the month. Healthcare, Consumer Staples, and Utilities each outperformed more growth-oriented areas such as Technology, Communication Services, and Consumer Discretionary.

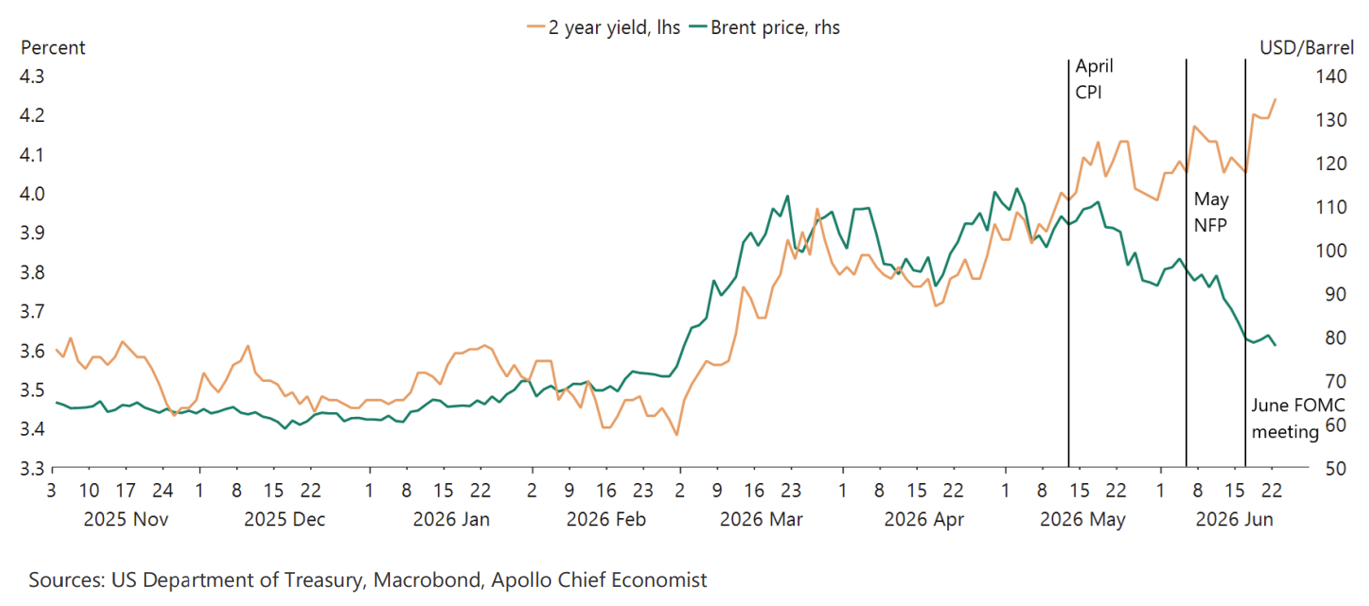

- Oil prices have pulled back sharply following optimism around a potential end to the war, correcting to near $70.00 per barrel, more than a third below their March peak, though still modestly above pre-war levels. Natural gas has followed a similar path, though European prices remain roughly 33 percent above where they stood before the conflict began. In the U.S., average national gasoline prices are trending back toward $4.00 per gallon. Even so, the retreat from peak energy prices does not signal that the inflation shock has passed.

- Airline stocks have been a notable beneficiary of the recent decline in oil prices. As measured by the NYSE Arca Airlines Index, the sector has now recovered the losses suffered in the wake of the Iran conflict, when surging jet fuel costs pressured margins across the industry. Fuel is among the largest and most volatile cost items for airlines, making the oil price retreat particularly meaningful at a time when consumer demand for flying has stayed intact.

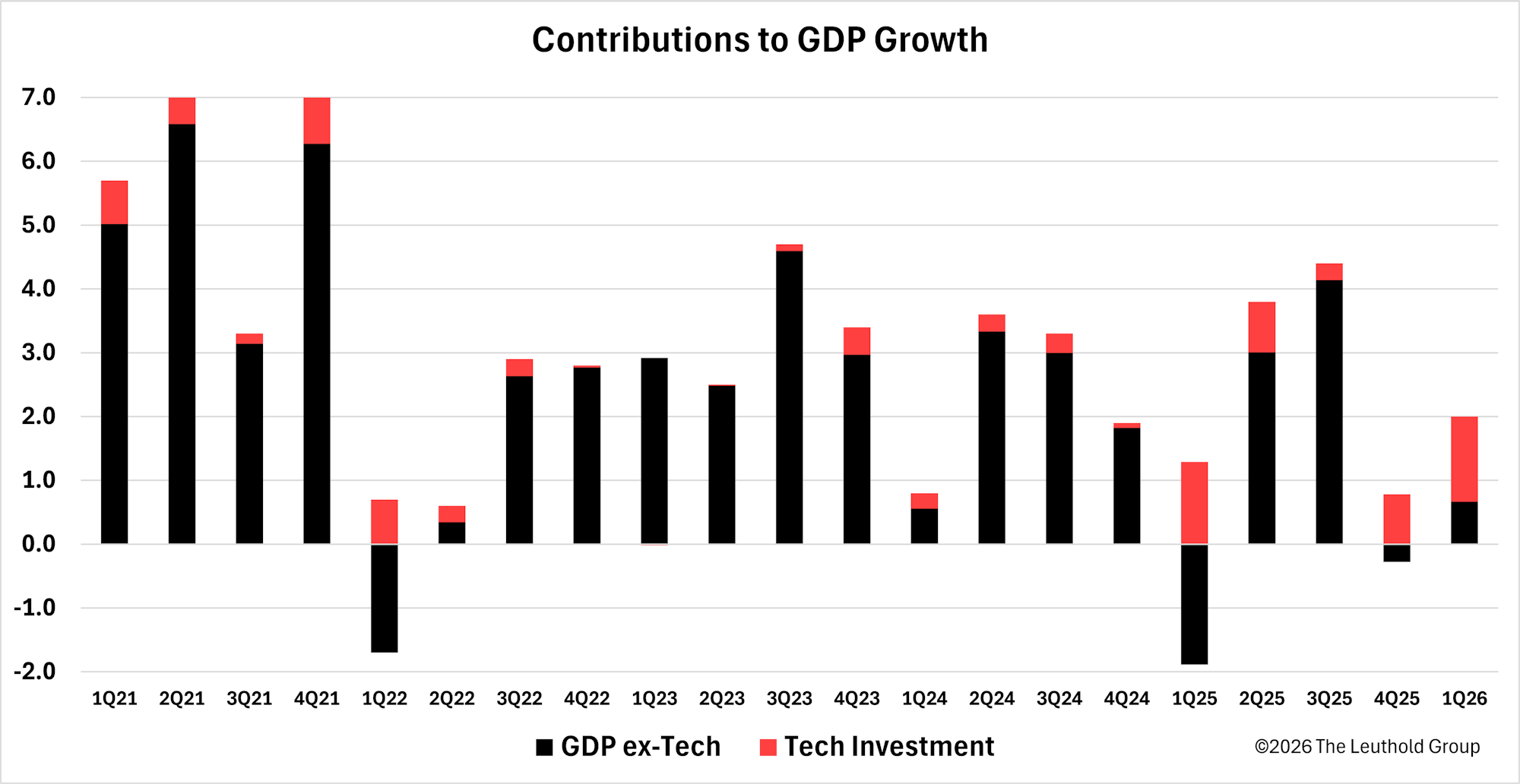

Technology’s contribution to GDP growth has been massive, accounting for two-thirds of first quarter growth and essentially all of the prior quarter’s modest gains, driven largely by surging investment in AI infrastructure, software, and information processing equipment. However, this growth is notably narrow, as the broader non-tech economy has softened meaningfully compared to the prior five years. We are cautious about interpreting today’s AI-driven spending boom as a sign of widespread economic strength, since overall GDP resilience is increasingly dependent on continued AI capital expenditure. With AI spending plans climbing even higher into 2027, the trend may continue for now, but similar to some of the dynamics in the stock market, concentrated growth of this kind carries real risk if investment slows due to power constraints, execution challenges, or shifting return expectations.

The market narrative is shifting in an important way: falling oil prices, rather than being seen as a relief from inflation, are now viewed as fuel for an already strong economy, potentially driving prices even higher. This shift has been driven by strong April and May Consumer Price Index releases (a key measure of inflation), a better than expected May jobs report (May Non-Farm Payrolls, which tracks the total number of paid workers in the U.S. economy excluding farm employees), and a Federal Reserve that has signaled it is in no rush to cut interest rates. As a result, markets now believe that the reopening of the Strait of Hormuz, while positive for energy supply, could further stimulate economic activity and push the Fed to raise interest rates sooner than previously expected.

Global markets navigated a complex month in June, defined by three overlapping themes: easing energy prices, renewed Federal Reserve resolve on inflation, and mounting skepticism around artificial intelligence valuations. The Memorandum of Understanding reached around the Iran situation reduces the near-term risk of conflict-driven economic disruption, though the truce remains fragile, and it is still unclear whether key regional parties will fully embrace the agreement over the long term. Stock prices remained volatile despite the relief in oil prices. Although lower oil prices could provide some relief within inflation numbers as well, the market is still unlikely to count on falling interest rates as a meaningful tailwind. At its most recent meeting, chaired for the first time by Kevin Warsh, the Fed held rates steady but shifted its messaging significantly. Updated projections now suggest rates are more likely to move higher before year-end, a notable reversal from earlier expectations of cuts. Nine of eighteen officials now forecast at least one rate hike in 2026, reflecting concern over inflation that reached 4.2% year-over-year in May (measured by the Consumer Price Index), its highest reading since 2023. For stock prices, these factors have left a mixed picture. Pockets of the market have been outperforming, but the tech behemoths that have been generating a significant amount of the market momentum the past 12 months have begun to slow. Investors are growing more skeptical about the near-term payoff from massive AI infrastructure spending. Questions around overcapacity, rising AI-related costs, and competition from cheaper models have weighed on sentiment. As a result, the S&P 500 is down 2.10% in June as of 6/29. We remain cautiously optimistic about the existing bull market, but have not been chasing this narrow momentum in markets. We have remained more diversified outside of just the AI narrative. One of those key areas has been international, which may begin to recover following the outsized pressure stemming from the war.

The purpose of the update is to share some of our current views and research. Although we make every effort to be accurate in our content, the data is derived from other sources. While we believe these sources to be reliable, we cannot guarantee their validity. Charts and tables shown above are for informational purposes, and are not recommendations for investment in any specific security. Forward-looking statements are based on current expectations and assumptions and are subject to risks and uncertainties that may cause actual results to differ materially.