Our current stock allocation is in an Over Weight position. This allocation of stocks vs. bonds is driven by technical market signals. These signals may lead to a shift in stock weightings in SFMG portfolios’ target allocations. This is not meant to be a specific allocation recommendation as this may vary across client portfolios.

- In a 6–3 decision, the U.S. Supreme Court struck down President Donald Trump’s use of emergency powers to impose tariffs on imports, leaving the question of refunds for previously collected tariffs unresolved. Shortly after the ruling, President Trump issued a proclamation under Section 122 of the Trade Act of 1974, imposing a 10% tariff on foreign goods for 150 days beginning February 24, with the possibility of raising the rate to 15%.

- The ISM Manufacturing Index rose to 52.6 from 47.9, returning to expansion for the first time in 10 months, with broad gains in new orders, production, and backlogs pointing to firm demand. The improvement was partly driven by increased capital spending as companies take advantage of restored 100% bonus depreciation incentives. Overall, the rebound suggests the industrial sector is stabilizing after a period of high rates and trade uncertainty.

- Retail sales were flat in December, missing expectations after a solid November gain, suggesting consumer spending cooled following a strong start to the holiday season. The report was delayed due to the government shutdown. The three-month annualized growth rate slowed to a 10-month low and fell below inflation, indicating a decline in real retail sales. While tax refunds may provide a temporary boost in spring 2026, softer labor market conditions, slowing wage growth, and weaker confidence point to more moderate consumer spending growth this year compared with last year.

- Despite headlines suggesting foreign nations may be shunning the U.S., the data tell a different story. Foreign investors more than doubled their net purchases of U.S. stocks in 2025, totaling $720.1 billion, up 134% from $307.5 billion in 2024, according to U.S. Treasury Department data released Wednesday. Overall, net foreign investment in long-term U.S. financial assets—including stocks and bonds—rose to $1.55 trillion in 2025 from $1.18 trillion the year before.

- Silver’s long streak without a major correction ended last week with a roughly 25% drop on 1/30/26—the third-largest single-day decline since 1968. The peak-to-trough drop in the iShares Silver Trust (ticker SLV) this year was -37.15%, from 1/28/26 to 2/17/26. Historically, similar breaks after all-time highs have marked the start of deep drawdowns, with average losses near 65% and recoveries often taking over a decade. While past episodes, particularly 1980, skew averages, the current cycle resembles that period, suggesting regaining recent highs may be a long, challenging process.

- The Dow Jones Transportation Average, which tracks 20 major trucking, airline, railroad, and shipping companies, is up 13% year to date, compared to just 0.36% for the S&P 500. Strength in transportation stocks is often viewed as a positive economic signal, as travel and goods movement remain essential regardless of broader market themes like AI. Notably, the rebound in trucking stands out. Combined with a strong January reading in the ISM Manufacturing Index, the gains in transportation suggest encouraging momentum for the broader economy.

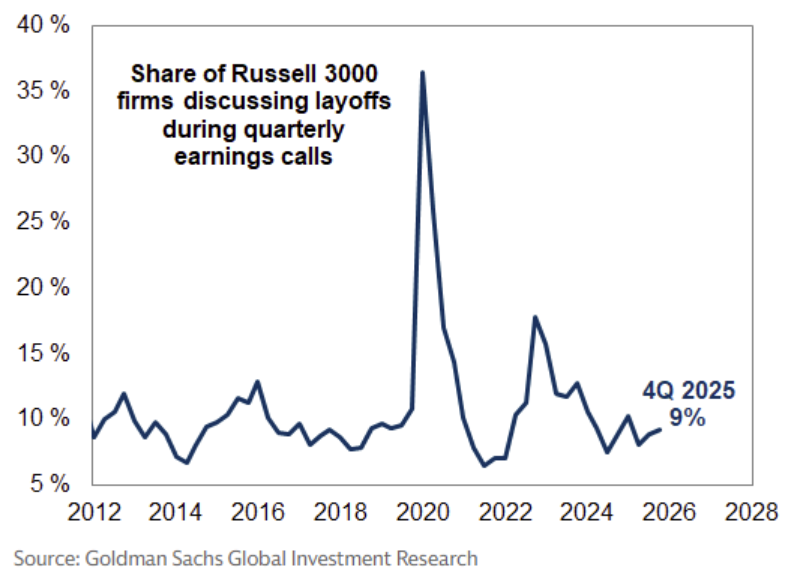

Labor market data is sending mixed signals. Corporate discussions of layoffs on earnings calls remain limited, consistent with stable weekly jobless claims and a solid January payroll report. However, job openings fell to 6.5 million in December—the lowest level since September 2020 and well below expectations—signaling softer labor demand. In addition, substantial revisions reduced last year’s job growth to 181,000, the weakest since 2020 and significantly below the previously reported 584,000. Overall, the labor market appears to be in transition—openings are shrinking, but employers are still filling roles, creating a low-hire, low-fire environment.

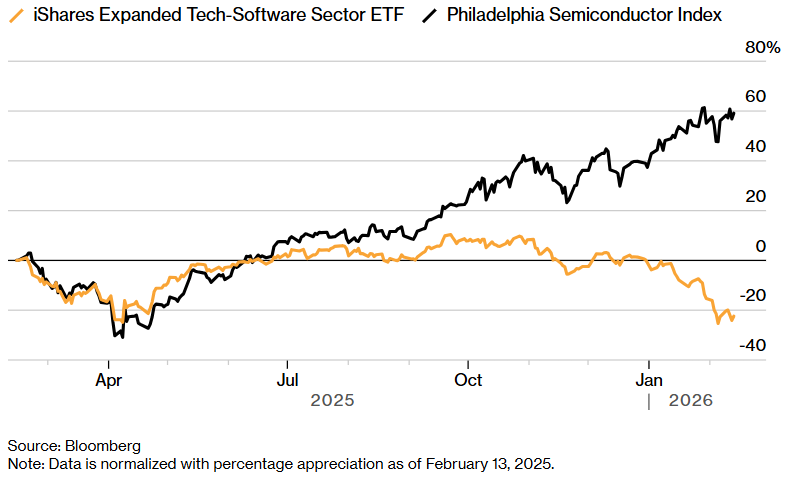

In 2026 YTD, semiconductors have materially outperformed software, with the PHLX Semiconductor Index up roughly 14% while broad software ETFs like IGV are down just over 20%. Semiconductor strength has been driven by sustained AI infrastructure and memory demand, whereas software’s underperformance reflects a broader rotation — elevated valuations and fears that AI will cannibalize existing software platforms have weighed heavily on the sector. Most recently, Anthropic’s launch of new AI productivity tools has deepened the software selloff, raising concerns that products offered by legal, data, and enterprise service companies could be quickly made obsolete. Currently, traders appear to be taking a “sell first, ask questions later” approach to the disruption narrative — though longer-term strategists are notably revising earnings estimates higher amid the selloff, suggesting the market may be pricing in more pain than the fundamentals ultimately warrant.

While peak uncertainty may have passed with April 2025’s tariff announcements, the Supreme Court’s ruling and the administration’s pivot to Section 122 tariffs has introduced fresh confusion and threatens to slow future trade deal progress. Notably, foreign nations are beginning to observe that countries which struck deals with the U.S. — the U.K., Japan, the U.A.E., and Australia — are now comparatively worse off than those who did not, such as China, Brazil, and Indonesia. This dynamic is likely to prompt renegotiations, the unwinding of unsigned agreements, and a broader push by foreign nations to forge free trade deals that exclude the U.S. altogether. In the near term, the uncertainty could slow or freeze decision-making — there is little incentive, for example, for a foreign airline to take delivery of a Boeing jet when waiting six months could save tens of millions of dollars. That said, we don’t expect the average U.S. effective tariff rate to rise materially ahead of the November midterm elections, given the political sensitivity around affordability and the administration’s desire to keep inflation in check. More broadly, the market is navigating a delicate balance: a resilient economy, softening labor conditions, AI enthusiasm, and a Fed on pause. The prevailing narrative remains centered on a near-perfect outcome — a soft landing, strong earnings growth, AI-driven productivity gains, and a tailwind from last year’s three rate cuts. But elevated valuations and high expectations leave little room for error, and disappointment on any front could trigger a meaningful selloff. Key risks include data that challenge the soft-landing thesis, renewed scrutiny around Artificial Intelligence’s return on investment, and continued policy volatility. The outlook remains constructive, but downside risk is elevated should confidence in that narrative begin to erode.

The purpose of the update is to share some of our current views and research. Although we make every effort to be accurate in our content, the data is derived from other sources. While we believe these sources to be reliable, we cannot guarantee their validity. Charts and tables shown above are for informational purposes, and are not recommendations for investment in any specific security. Forward-looking statements are based on current expectations and assumptions and are subject to risks and uncertainties that may cause actual results to differ materially.